There are places on the world map whose significance far exceeds their geographic size. The Strait of Hormuz is one of them. A narrow stretch of water between Iran, Oman, and the United Arab Emirates determines the stability of global energy supply every single day. Roughly one fifth of the world’s oil consumption passes through this corridor, making it one of the most critical logistical chokepoints in the international economic system.

From the perspective of the Gulf region, the Strait of Hormuz is far more than a shipping route. It is a strategic artery of the globalized economy. In times of rising geopolitical tensions—particularly amid the escalating confrontation between Iran, Israel, and the United States up to 2026 the narrow passage has once again become a focal point of international attention.

Geographically, the strait connects the Persian Gulf with the Gulf of Oman and ultimately the open waters of the Arabian Sea. Iran controls the northern coastline, while Oman, through the Musandam Peninsula, and the United Arab Emirates form the southern boundary. At its narrowest point, the strait measures only about 33 to 40 kilometers across. For maritime navigation, however, the usable space is much smaller. International shipping operates through a traffic separation scheme consisting of two shipping lanes, each roughly three kilometers wide one for incoming traffic and one for outgoing vessels—separated by a buffer zone of similar size.

Chokepoint of Energy Transportation

Unlike artificial waterways such as the Suez Canal, the Strait of Hormuz is deep enough to accommodate the largest oil tankers in the world, the so-called Very Large Crude Carriers (VLCCs). The deep-water channels required for these vessels run largely through Omani territorial waters, which adds another layer of strategic complexity to the geography of the region.

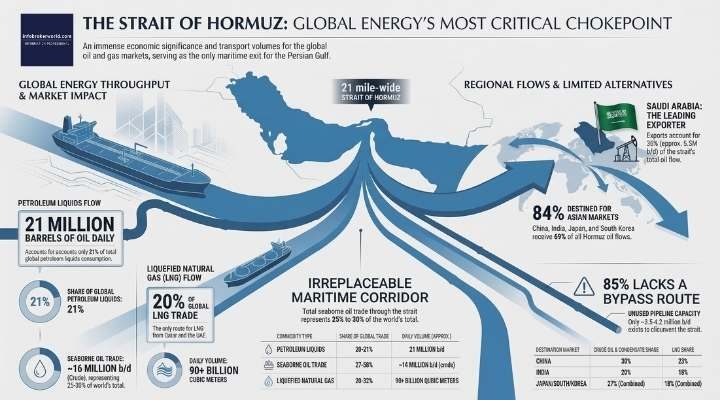

The true importance of the strait becomes clear when examining the economic data. On average, around 20 to 21 million barrels of crude oil and petroleum products pass through Hormuz every day. This represents roughly 20 percent of global oil consumption and nearly 30 percent of all seaborne oil trade worldwide. In addition to oil, the strait also plays a central role in the global liquefied natural gas market. Approximately 20 percent of global LNG trade passes through these waters, primarily exports from Qatar and the United Arab Emirates. In financial terms, the annual energy flows moving through this corridor are estimated to be worth between 500 and 600 billion US dollars.

Saudi Arabia is the largest exporter relying on this route, shipping roughly 5.5 million barrels of oil per day through the strait about 40 percent of the total Hormuz oil flow. Other key exporters include Iraq, the United Arab Emirates, Kuwait, and Iran.

While Europe and the United States would feel the consequences of disruptions primarily through higher global energy prices, the physical dependency lies largely in Asia. Between 82 and 84 percent of oil exports and roughly 83 percent of LNG shipments passing through the Strait of Hormuz are destined for Asian markets. China, India, Japan, and South Korea together account for nearly 70 percent of these energy flows. China, for example, imports around 90 percent of Iran’s oil exports, while India receives between 40 and 66 percent of its crude oil imports and roughly 60 percent of its gas imports through this corridor. The energy security of many Asian economies is therefore closely tied to the stability of this maritime passage.

The question of alternative routes is often raised, yet the available options remain limited. Some pipeline systems partially bypass the Strait of Hormuz, but their capacity is relatively small compared to the volume of daily shipments. Saudi Arabia operates the East-West Pipeline, also known as Petroline, which connects the country’s eastern oil fields with ports on the Red Sea and has a maximum capacity of about five million barrels per day. The United Arab Emirates operates the Abu Dhabi Crude Oil Pipeline, which transports oil from Abu Dhabi’s fields to the port of Fujairah on the Gulf of Oman, with a capacity of roughly 1.5 to 1.8 million barrels per day. Combined, these alternative routes could redirect approximately 3.5 to 4.2 million barrels per day in a crisis scenario. Compared with the more than 20 million barrels that normally pass through Hormus each day, it becomes clear that even under optimal conditions less than a quarter of the supply could be rerouted.

Vulnerable shipping route

The vulnerability of this region is not new. During the Iran-Iraq War in the 1980s, the Persian Gulf experienced what later became known as the “Tanker War.” Both sides systematically targeted oil infrastructure and commercial vessels. More than 400 ships were attacked during the conflict, over 60 percent of them oil tankers, and around 400 sailors lost their lives. In response, the international community began protecting commercial shipping. In 1987, the United States launched Operation Earnest Will, reflagging Kuwaiti tankers under the US flag so they could be escorted by American naval forces. Despite hundreds of attacks, however, one fact remained constant: shipping through the Strait of Hormus was never completely halted. The reason was largely economic every party involved depended on the continued flow of oil revenues.

Podcast: Strait of Hormuz – Transition Middle East

In recent years, geopolitical tensions in the region have intensified again. The Strait of Hormuz has increasingly become part of a broader confrontation involving Iran, Israel, and the United States. In April 2024, Iran’s Islamic Revolutionary Guard Corps seized the container ship MSC Aries in the region. In June 2025, US and Israeli airstrikes targeted Iranian facilities, including nuclear infrastructure. Further escalations in February 2026 heightened tensions even more. The Iranian parliament symbolically voted in 2025 in favor of closing the Strait of Hormuz, although the final decision rests with the country’s Supreme National Security Council. By late February 2026, Iranian Revolutionary Guard units had reportedly warned some vessels via radio that passage through the strait was temporarily “not permitted,” leading to heightened uncertainty and route changes among several tankers.

A complete military blockade of the strait would be complex but not impossible. Iran possesses several tools for asymmetric naval warfare, including an estimated 6,000 naval mines, fast attack boats, submarines, and coastal anti-ship missile systems. Even the threat of mining the strait could have serious consequences. War-risk insurance premiums for tankers would likely surge, and shipping companies might begin avoiding the route altogether.

The global economic implications of such a disruption would be significant. Energy market analysts estimate that even a temporary interruption of shipping could drive oil prices sharply higher. Many projections suggest that crude oil prices could spike to between 120 and 150 US dollars per barrel—or even beyond—in a severe crisis scenario. Such a surge would increase transportation and production costs worldwide, intensify inflationary pressures, and potentially trigger a global economic slowdown.

At the same time, a closure of the Strait of Hormuz presents a strategic paradox for Iran itself. The country exports the vast majority of its oil through this very route, primarily to China. Blocking the strait would therefore cut off its own primary revenue stream. Former US Secretary of State Marco Rubio described such a move as “economic suicide” for the Iranian leadership. It would also place significant strain on relations with key trading partners—most notably China, which relies heavily on Iranian crude imports.

The Strait of Hormuz therefore remains one of the most sensitive strategic nodes in the global economy. When tensions escalate in this region, the consequences ripple across the world—from energy prices and inflation to supply chains and financial markets. A complete closure of the passage remains unlikely because the economic costs for all parties would be enormous. Yet history shows that the mere possibility of disruption is often enough to move global markets.

Or, to put it differently: a stretch of water less than forty kilometers wide regularly determines the stability of a multi-trillion-dollar global energy system.